Key staff and all directors need to know about the money story, even if your corporation has an in-house accountant or a bookkeeper.

This Oracle is aimed mainly at directors but will be useful for anyone wanting to know more about managing a corporation’s money.

Good governance depends on good financial management

Plan what yourcorporation can afford to do—prepare a budget.

Plan what yourcorporation can afford to do—prepare a budget.- Set policies and procedures for handling money—to minimise risks.

- Keep good records—so your money story is up-to-date, accurate and correctly records the corporation's financial transactions.

- Monitor the money story using financial reports—to make sure your corporation is on track and can pay its bills.

Directors are accountable

The ultimate responsibility for a corporation’s money story always rests with the directors. Employees look after the day-to-day finances, but it’s the directors who make the decisions, and are responsible under the Corporations (Aboriginal and Torres Strait Islander) Act 2006 (CATSI Act) if something is not done correctly or if the corporation is insolvent (unable to pay its bills).

So the directors can’t just take the word of the staff that things are going well, or say it’s someone else’s job to look after the money story. It’s absolutely essential that they check the corporation’s money story and make sure it can pay all of its bills. Only then can the directors make good decisions for the corporation.

Help for directors

If your directors lack skills and experience in financial management, they could appoint an independent director with an accounting or finance background, or hire an accountant or bookkeeper as a staff member or adviser.

An independent director with relevant qualifications can strengthen both a board of directors and the corporation. Make sure it’s someone able and willing to share their knowledge. Find a skilled person through Independentdirectory.

If you’re hiring an accountant or bookkeeper, check their experience and qualifications, and talk to their referees. You need someone you can trust to manage the money story and to tell the directors of any problems as soon as they arise.

Warning signs of poor financial management

- any large expenses not expected or approved

- overdue bills or loan repayments

- people owed money asking when they’ll be paid

- your accountant, bookkeeper or treasurer cannot produce reports on the money story

Your money story has many parts

Think about your whole money story—from planning and spending to monitoring and reporting.

Policies and procedures

In corporations with many activities and staff, it’s not practical for directors to sign off on every payment. Instead, the board may agree on which staff can sign contracts or approve spending—and how much. These are known as financial delegations. Once the board approves the delegations, particular staff are empowered to approve and spend the corporation’s money within their limits and in line with the budget.

Make sure all staff know about their delegations. Directors should review financial delegations at least once a year in case they need to change.

Depending on the size and complexity of your corporation, you might also need policies and procedures to safeguard against over-spending, and to prevent errors and fraud. For example:

- the same person should not propose spending and then approve it

- you may require at least two delegated people in the corporation to approve payments, whether by cheque or electronic funds transfer (EFT).

Budget

A budget lists all your sources of income and the expenses you anticipate.

Preparing a budget enables you to work out what the corporation can afford to do; determine if it has enough money to pay for the things it needs to pay; and (if there’s money left over), prioritise things that are most important and needed for the corporation.

In preparing a budget you might consider:

- Will you receive new or reduced funding or have extra costs in the upcoming year?

- Do you need to buy any large assets, such as a building, or fleet of vehicles or computers?

- Can you reduce the corporation's costs, or increase its income?

Transactions

(tap the image to enlarge)

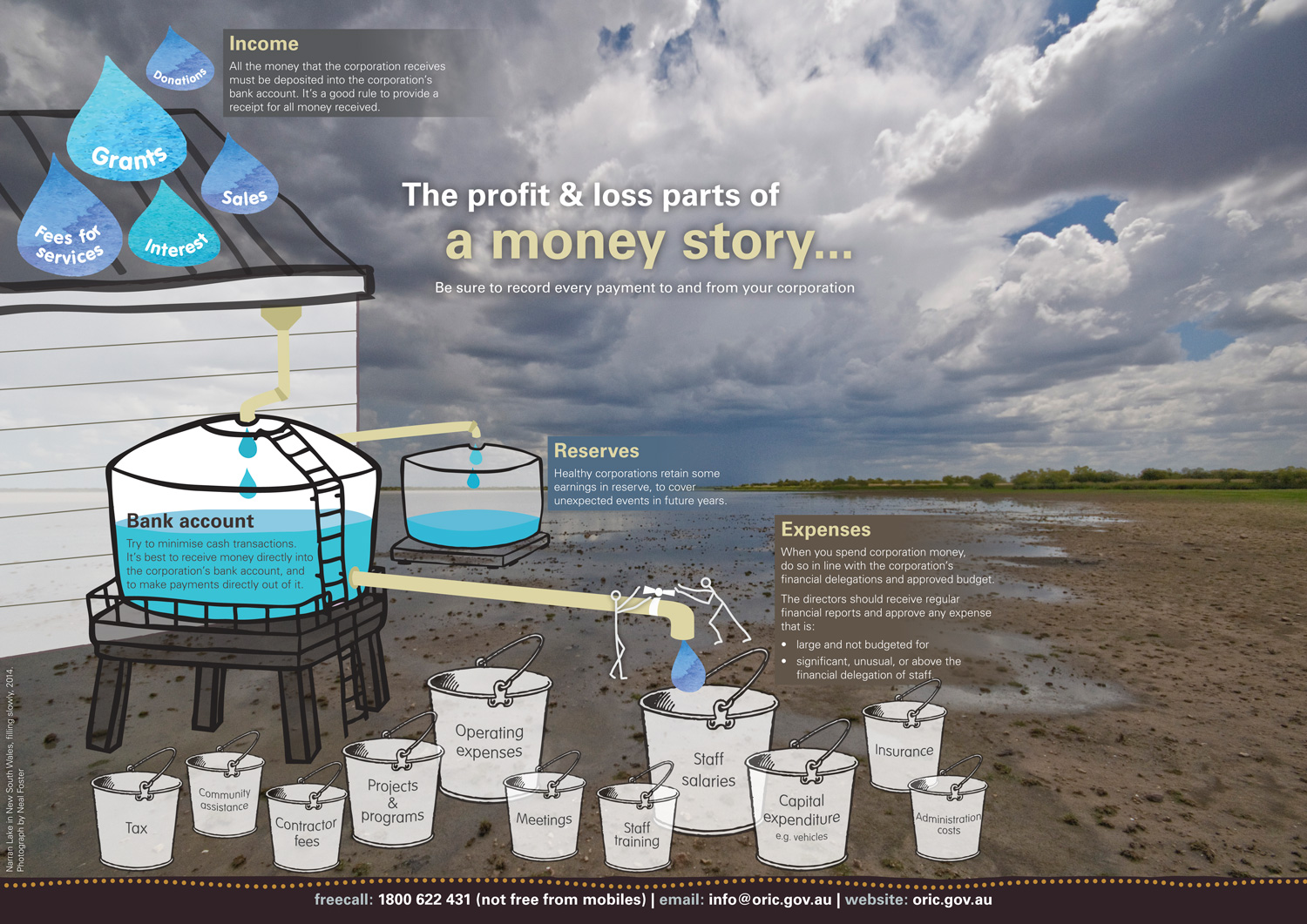

Income

All the money that the corporation receives must be deposited into the corporation’s bank account. It’s a good rule to provide a receipt for all money received.

Bank account

Try to minimise cash transactions. It’s best to receive money directly into the corporation’s bank account, and to make payments directly out of it.

Reserves

Healthy corporations retain some earnings in reserve, to cover unexpected events in future years.

Expenses

When you spend corporation money, do so in line with the corporation’s financial delegations and approved budget.

The directors should receive regular financial reports and approve any expense that is:

- large and not budgeted for

- significant, unusual, or above the financial delegation of staff.

Monitoring and reporting

Day-to-day

Your corporation needs to know that every transaction (payment and receipt) is valid and approved. The task of checking the bank statements (reconciling the bank accounts) should be done by someone who is not involved in spending or receiving money.

At each directors’ meeting

Directors must take time to read and understand the financial reports and how your money story has changed from month to month. If you have any doubt about what it means, ask someone with financial skills to talk it through with you.

A profit and loss statement (also called the P&L, an income and expenditure statement or a statement of financial performance) is a way to keep track of how your corporation is performing. It shows:

- income or revenue received/earned for the month in each category (e.g. grants, donations, fees for service, sales and interest)—this is money coming in

- expenses incurred in that month (e.g. wages, utilities, taxes, fees.)—this is money going out

- the net result (income minus expenses, resulting in a net surplus or loss)—this is what’s left.

If your P&L is prepared with a column for each month showing both actual and budgeted income and expenditure, it’s easy to see if your money story has taken a dramatic turn or if it’s business as usual.

A balance sheet (also called a statement of financial position) shows what a corporation owns and owes at a point in time. It includes:

- assets—what your corporation owns, including money in the bank, money owed by people to the corporation (debtors), land and property, vehicles and equipment

- liabilities—what your corporation owes to others, including bank loans, money owed to people (creditors) and unpaid taxes

- equity—how much your corporation is worth (assets minus liabilities).

Your corporation’s bottom line is how much it has (income and assets) minus how much it owes (expenses and liabilities). To be solvent, your bottom line must be above zero.

At the annual general meeting

Remember to share your audited financial reports with members. At the annual general meeting (AGM) members are entitled to hear about the money story and ask questions.

Also at the AGM, if a corporation is required to lodge audited financial reports with the Registrar, members need to appoint an auditor for the next year, and to agree on their fee. An auditor is an independent assessor who checks if your financial statements tell a full and accurate money story in accordance with the CATSI Act and accounting standards.

Help shape ORIC’s service

To better manage its money, what does your corporation need?

Please respond to our quick survey – so we can help Aboriginal and Torres Strait Islander corporations like yours.

Indigenous Accountants Australia

Indigenous Accountants Australia (IAA) supported the development of this issue of the ORIC Oracle. IAA is a joint initiative of CPA Australia and Chartered Accountants Australia and New Zealand.

We aim to attract more Aboriginal and Torres Strait Islander people to pursue a career in accounting—as a pathway to economic empowerment and financial self-sufficiency.

We do this by providing support to students and connecting them with their peers and professional networks.

We believe that boosting the number of Indigenous accountants is pivotal to promoting financial literacy and economic development in Aboriginal and Torres Strait Islander communities.

Avoid a breach

Lodge online now—avoid breaching your 2015–16 reporting requirements. The Registrar may take legal action against your corporation if you fail to lodge your reports.